1. Information for Foreign Entrepreneurs starting business in Korea about taxes on foreign invested companies or the place of business of foreign corporate in Korea

-

(1) Foreign invested company

To be recognized as FDI, foreign direct investment, the investment amount should be KRW100 million or more per foreigner and the foreigner should own at least 10 percent of either the total number of voting stocks issued by a Korean corporation or total equity investment. Under the law of foreign investment promotion act foreign investors shall notify foreign investment to enjoy entitlements including tax support.

-

(2) Permanent establishment of foreign corporation

If a nonresident has a fixed place to carry out all or part of the business in the Republic of Korea, he/she shall be deemed to have a domestic place of business. Permanent establishment include:

Branch, office or place of business; a store or other fixed sales places; a place of work, factory or warehouse; a place of construction, site of construction, assembly or installation work, or a place where supervision is conducted in relation thereto, which continues to exist exceeding six months; any of the following places where services are provided by employees

2. Taxation based on existence of permanent establishment

-

(1) with permanent establishmen

For profits generated from the establishment domestic taxation system will be applied as a form of composite income tax for a nonresident individual and of corporate tax for a foreign corporation.

-

(2) without permanent establishment

For income from domestic sources any nonresident or foreign corporation is not liable for withholding tax because withholding agent pays the tax when the wages are paid. Where a withholding agent pays wages to a nonresident or foreign corporation he or she should check whether the taxes on the wages should be levied based on domestic taxation system or tax treaties.

When the two conflicts, trade treaties override domestic taxation system which carry lower reduced tax rates.

3. Taxation not based on international tax treaties

Where income from domestic sources occurred to any nonresident and corporation with no fixed establishment withholding taxes will be levied based on the provisions of income tax law and corporate tax law respectively. In this case, withholding tax agent will pay the tax based on withholding tax rates for nonresidents and foreign corporations.

Korean tax law stipulates withholding tax rates for nonresidents and foreign corporations are as follows:

| Interest income |

20 percent of the payment |

| Dividend income |

20 percent of the payment |

| Ship rental income & business income from domestic sources |

2 percent of the payment |

| Personal service income |

20 percent of the payment |

| Capital gains |

Less amount between the 10 percent of sale proceeds and 20 percent of gains on transfer |

| Royalty income |

20 percent of the payment |

| Income from transfer of securities |

Less amount between the 10 percent of sale proceeds and 20 percent of gains on transfer |

| Miscellaneous income |

20 percent of the payment |

4. Taxation based on international tax treaties

As of June, 2018 South Korea has entered into tax treaties with 93 countries, pursuing to offer tax benefits to member states of the treaty. In most cases international tax treaties override domestic tax laws in many cases. Under the treaties reduced tax rates, limited tax rates, are applied. Limited tax rate means the maximum tax rate at which a resident or corporation of the other contracting country may be taxed under international tax treaties. Every country has different tax treaties each other but overall the treaties stipulate that interest income, dividend income, royalties, and personal service income should be levied between 10 to 15 percent.

Examples of tax rates on international treaties

| U.S. |

· Local income tax should be additionally imposed

· Interest income: 12%

· Dividend income: 10% for holding more than 10% of shares, 15% for other cases

· Royalty income: 10% for films with copyright, 15% for other cases

· Personal services: offering services for a period or periods not exceeding in the aggregate 183 days, earning profits exceeding $3,000 it is taxable in a contracting state |

| China |

· Interest income: 10%

· Dividend income: 5% for holding more than 25% of shares, 10% for other cases

· Royalty income: 10%

· Personal services: offering services for a period or periods not exceeding in the aggregate 183 days, it is taxable in a contracting state |

| Japan |

· Interest income: 10%

· Dividend income: 5% for holding more than 25% of shares, 10% for other cases

· Royalty income: 10%

· Personal services: offering services for a period or periods not exceeding in the aggregate 183 days, it is taxable in a contracting state |

| Vietnam |

· Interest income: 10%

· Dividend income: 10%

· Royalty income: 5% of the royalties for patent right, license for drawing, confidential process, industrial, commercial, academic experience or equipment. 10% for other cases

· Independent personal services: independent services without fixed base are taxable in a contracting state

· Dependent personal services: in case of offering services for more than 183 days, it is the subject to taxation from the contracting country |

5. Taxation Process of foreign Corporations in Korea.

| Process 1 |

Where income of a foreign corporate occurs it should be decided whether the income is taxable under the Korean tax law. If it is international tax treaties also should be considered as the next step. However the income is not the subject to income tax if it is not taxable under the Koran tax law nor international tax treaties. |

| Decide whether the income is taxable |

| Process 2 |

In case of taxable income the source of income should be considered. Where the income was generated from domestic place of business the income is the subject to composite income tax. Provided that the income did not come from domestic place of business the income is the subject to withholding tax under separate taxation. However, capital gains are not the case for this. |

| Decide how to levy taxes |

| Process 3 |

Where domestic tax rates are lower than those of international tax treaties tax should be levied based on domestic tax rates. In the case of the opposite, tax rates of international tax treaty should be applied. |

| Decide applicable rates under separate taxation system |

7. Procedures necessary to be informed to new foreign corporations

-

1. Hometax System:

after subscribing to Hometax system, Korea's online tax administration service, acceptance of delegation is needed in order to let the tax agent sign in with client's ID and Password to have an access to his or her tax information.

-

2. Cash Receipt System:

Clients should be well-informed about cash receipt system especially about penalties imposed on businesses which are required to become a Cash Receipt merchant but fail to become a Cash Receipt merchant or refuse to issue cash receipts.

-

3. Four Key Insurance policies of Korea:

an overview of Korea's social insurance system should be offered.

Ⅰ. A Guide on Basic Operation Process for new Client

(Tax filing services for FDI and Domestic Place of Business of Foreign Corporation)

VAT (Value Added Tax)

1. Period & Tax filing due date

| ① The 1st half Period Preliminary |

(Jan-Mar) file & pay by Apr 25 |

| ② The 1st half Period Final |

(Apr-Jun) file & pay by July 25 |

| ③ The 2nd half Period Preliminary |

(Jul-Sept) file & pay by Oct 25s |

| ④ The 2nd half Period Final |

(Oct-Dec) file & pay by Jan 25 of next year |

2. Structure

VAT received (Output tax amount)

- VAT paid (Input tax amount)

= VAT payable tax amount (' + ' payable, ' - ' refundable)

-

(1) Output tax amount: 10% of ‘Value of supply' for sales of goods or services

1) Value of supply in Tax invoices

(Aggregate Tax Invoices for Individual Suppliers are required to be submitted)

2) the List of Total output tax invoice are required to be submitted)

3) Value of supply in the Credit card slips

4) Value of supply in the Cash receipts

5) Value of supply of the lot-solid verified by the lot-solid table

6) And other Value of supply which are verified by each evidential document

-

(2) Input tax amount: Input tax amount on goods or services provided

1) Input tax amount in Tax invoices

(Aggregate Tax Invoices for Individual Creditors are required to be submitted)

2) The deemed input tax amount :

- deduction rate: 2/102

- corporation in restaurant business: 6/106

- individual business operator: below KRW 200mil on tax base : 9/109, over KRW 200mil: 8/108

3) Input tax amount in the Credit card slips for tax deduction

- Any credit card slip issued by general taxable individuals

- The amount of business credit card spending shall be checked on 『Hometax system』 before filing VAT return. (Credit card bills should be submitted to the agent of tax accounting firm)

4) Input tax amount deemed to be excluded from tax deduction

- Any Credit card slip issued by simplified taxable individuals

- On disbursement which are not directly related to the business

- The purchase, lease and maintenance of non-business automobiles

- Certain expense items related to entertainment

3. Evidential Documentary Management

-

(1) All figures on the following documents should correspond to each other

- Contract document, transaction statement, estimate sheet

- Sales tax bill, purchase tax bill, export certificate, domestic credit

- Disbursement voucher demonstrating trading value such as deposit slip, remittance receipt, giro payment slip

-

(2) Tax invoice must be archived separated from other evidential documents because it is highly likely to be omitted in the process of filing for VAT return.

4. Check for VAT ratios by the types of industry

-

(1) As the Korean tax law applies different VAT ratio by the types of industry average VAT ratio in one's industry and VAT ratio of the previous year should be checked before filing for VAT return.

-

(2) The balance between card sales and cash sales should be monitored.

-

(3) Variations in the proportion of card sales and cash sales should not be large.

5. Report management

6. Classification of taxable supplies and tax-free supplies by items

-

(1) Taxable supplies and tax-free supplies should be classified by items

-

(2) Check for Items exempt from deductions in input tax amount

- Input tax amount related to tax-free items

- Input tax amount related to entertainment expense

7. Reporting Sales of Exempted tax payers

-

(1) Report on ‘Present Status of Place of Business' is required to be submitted by February 10 of the following year of the relevant taxable period

Sales reporting of general tax payers & business operators falling both under general and exempted tax payers

-

(2) Filing VAT return – quarterly for corporations, half-yearly for individual business owners

Tips for Data Management

1. Sales & Purchase Data Management

-

(1) Contract document

- Business contractors agreement

- Delivery contract

- Transaction statement

- A written estimate

-

(2) Tax bill

-

(3) Documentary evidence for payment

- Business contractors agreement

- Deposit slip

- Payment list

- A bill receivable

2. Costs on evidential documents should be well-balanced. It should be closely monitored whether there are any materials omitted or filled out incorrectly.

WITHHOLDING TAX

Wage Income

1. Period & Tax filing due date

-

(1) Withhold (simplified) Income Tax from Monthly payroll (with local resident tax)

- file & pay by 10th of the following month

-

(2) Annual Tax adjustment

- file & pay by Mar 10 for the previous calendar year

2. Documents for personal services

-

(1) Payroll report on regular employee(s)

-

(2) Payment detail report on daily employed worker(s)

-

(3) Personal service payment detail statement for independent profession income(business income) or other income

3. Payroll Process for the employed employee

-

(1) Check Entry & Exit employee(s) with the effective date

Following document should be required for new employees

- 'Resident registration' of employee

- Employee personal data (name, registration number, address, family dependents, etc.)

- Employment contract or annual income contract

-

(2) Check the Salary (Remuneration) amount based on the contract

-

(3) Prepare the Payroll report. The report includes payment details, deductions details (taxes, deductions related to social insurances), and net payment

-

(4) Salary payout

-

(5) File and pay the withholding taxes by 10th of following month

4. Payment to the Daily employee worker(s)

-

(1) Check the list and each personal data should be secured (name and registration number, etc.)

-

(2) Check the payment amount

-

(3) Prepare the Payment report (non-taxable KRW150,000/day)

-

(4) Payout

-

(5) File and pay the withholding taxes by 10th of next month

5. Non-Taxable Items for the employed including

-

(1) Meal allowance - up to KRW100,000/month

-

(2) Car allowance - up to KRW200,000/month (applicable only to car owners)

-

(3) Childcare allowance - up to KRW100,000/month

-

(4) Night shift & Holiday overtime allowance for Production Field Direct employee up to

KRW2,400,000/year (applicable only for employee whose monthly salary is under KRW1,000,000)

6. Social Insurance Deductions

| |

National Pension

(NP) |

National Health Insurance

(NHI) |

Employment Insurance

(EI) |

Industrial Accident Comp Ins

(IACI) |

Employee portion

(deduct from monthly payroll) |

4.5% |

ⓐ NHI: 3.23% |

ⓐ Unemployment: 0.65% |

n/a |

| ⓑ Long-Term Care: 8.51% of NHI |

ⓑ Security etc: n/a |

| Employer portion |

4.5% |

ⓐ NHI: 3.23% |

ⓐ Unemployment: 0.65% |

0.7% ~ 3.2% ** |

| ⓑ Long-Term Care: 8.51% NHI |

ⓑ Security. Etc.: 0.25%* |

| Calculation based on |

Total Income

(standard table) |

Total Income

(standard table) |

Total Income |

Total Income |

| Remarks |

Ceiling amount for monthly standard

KRW4,490,000 |

|

* different based on the type of business

and/or number of employee |

** different based on the business category

and/or accident rate |

7. Withholding method on the Payment

-

(1) Monthly payroll – withhold the monthly income tax based on the “Simplified Tax Table”

-

(2) Independent profession income (business income) – withhold 3.3% (local resident tax included) of the total payment amount

-

(3) Other income – deduct the necessary expenses (80% of the total payment amount) and then, withhold 22% from that amount (local resident tax included)

-

(4) Personal service income for Non-resident – withhold 22% of the total payment (local resident tax included); Tax Treaty has priority

-

(5) Payment to the services which was occurred in the Overseas: no obligation for the tax withholding

-

(6) Royalties, Interest Income, Dividend income which were paid to the overseas from the domestic – The ceiling rate in Tax Treaties with each country shall be applied

CORPORATE INCOME TAX

1. Period & Tax filing due date

Business period (Jan. 1 ~ Dec. 31, or the period filed, or period designated by local authorities)

– file and pay within 3 months after the business period closing date

2. Taxable Income

| Accounting Book |

Corporate Tax |

Evidential Documents |

| Sales |

gross income |

(Sales) Tax invoice |

| Cost of goods (-) |

deductible expenses |

(Purchase) Tax Invoice (cost)

Payroll register (labor cost)

Appropriate Receipts (other costs) |

| Gross profit (=) |

|

|

| Sales & Admin expense (-f) |

deductible expenses |

(Purchase) Tax Invoice (cost)

Payroll register (labor cost)

Appropriate Receipts (other costs) * |

| Operating profit |

|

|

| Non-operating profit (+) (-) |

|

|

| Net income |

Taxable income for the business period |

3. Corporate Tax Rate

| 2018 ~ |

| Tax Base |

Rate (%) |

Amount of progressive deductions |

| Below KRW 200 million |

10% |

- |

Above KRW 200 million

~ below 20 billion |

20% |

20,000,000 |

Above KRW 20 billion

~ below 300 billion |

22% |

420,000,000 |

| Above KRW 300 billion |

25% |

9,420,000,000 |

Income Tax

1. Period & Tax filing due date

(1) File by May 31st of the following year

(2) Taxable period: January 1st ~ December 31st

2. Income Tax Rate

| 2018 ~ |

| Tax Base |

Rate (%) |

Amount of progressive deductions |

| Below KRW 12 million |

6% |

- |

Over KRW 12 million ~

below KRW 46 million |

15% |

1,080,000 |

Over KRW 46 million ~

below 88 million |

24% |

5,220,000 |

Over KRW 88 million ~

below 150 million |

35% |

14,900,000 |

Over KRW 150 million ~

below 300 million |

38% |

19,400,000 |

Over KRW 300 million ~

below 500 million |

40% |

25,400,000 |

| Over KRW 500 million |

42% |

35,400,000 |

3. Profit & Loss Structure

② Rental payment

- Purchase tax bill |

① Sales (profits)

confirmed by filing for VAT returns |

③ Labor expense

- Withholding tax return

- Four key social insurance

- Non-taxable income |

④ Expense

- Receipts prescribed by the Korean tax law

- Corporate credit card receipt

- Penalty taxes imposed for inadequate evidentiary documents

- Expenses with limitations |

⑤ Income (Income rate)

For personal business operator income rate is calculated as it follows: 1-(simple expense rate) |

4. Financial structure

| Asset |

Debt |

| ⑥ Suspense payment |

⑦ Debt Ratio |

| Capital |

⑧ Stocks for corporations

- In transferring stocks stock evaluation should be taken before transferring

- Share transfer agreement/ stock certificate contract

- Report changes of stocks: gift tax & capital gains tax

- Stockholder's list |

Taxable Income

In principle taxable income is calculated based on ledgers but in very rare cases such as losing or damaged ledgers the calculation is based on estimation.

1. Receipt and Keeping evidentiary Documents of Expenditures

-

(1) Any corporation must collect and keep all receipts for business expenses. In this case, receipts must be the ones prescribed by the Korean Tax law. If any business fails to collect and keep receipts for a business expense that exceeds a certain amount penalty taxes for inadequate evidentiary documents shall be

-

(2) Receipts prescribed by the Korean tax law include tax invoice, credit card receipt, cash receipt issued by Korean Cash Receipt merchant, receipt for giro bill payments.

-

(3) The expense that exceeds a certain amount means the expense that exceeds KRW 30,000 (as of 2008). This is mandatory for all corporations and individual business operators who earn annual income more than KRW 48 million.

-

(4) Otherwise, 2% of additional tax will be imposed

2. Tips for the Deductible Expenses

-

(1) The appropriate receipts should be secured for all Entertainment expenditure which is more than KRW10,000. Otherwise, it will not be regarded as deductible expenditure.

- Only the Corporate credit card receipt will be acceptable as appropriate receipt

- Exception; the expense for condolatory / congratulatory cases without appropriate receipts, it will be acceptable upto KRW200,000

-

(2) The deductible expense with limitation

- Entertainment

KRW24,000,000 + Sales revenue * 0.2%

; (small & medium size company) (Sales revenue under KRW10 billion) - Donation

; The donation during each business year, the amount in excess of 5% of the income amount

; (excluding donation amount and deficits of within ten years before) shall not be included in deductible expense.

-

(3) Rental expense

- Tax invoice for rental expense should be secured (if tax invoice could not be secured as the lessor is a ‘simplified taxpayer', the normal receipt should be secured. And the payment is required to be made via bank transfer.

- The payment should be made via bank transfer in case no tax invoice issued

-

(4) Other expenses

- Receipting and keeping evidentiary Documents of Expenditures is essential for all expenses to be acknowledged as deductible one.

- Spending resolution, credit card slip, tax invoice, credit card receipt issued by Cash Receipt merchant, giro receipt, remittance advice

3. Balancing overall expenses

-

(1) Balancing between expenses and cost ratio is important. Businesses should check whether their expenses make sense compared to average cost ratio. If it doesn't businesses should check their evidential documents whether there is any omission or wrong recording.

-

(2) Businesses should monitor the ratio of sales revenue to SG&A

-

(3) The ratio of labor cost to expense items related to labor cost such as welfare benefits or transportation cost

4. Corporate Credit Card

In order to be recognized as appropriate expense including entertainment expense, the Corporate Credit Card and/or Individual Corporate Credit Card should be used for all business related expense payment

5. Business Bank Account

All expenses are required to be paid through ‘Bank transfer' including Corporate Credit card expense settlement.

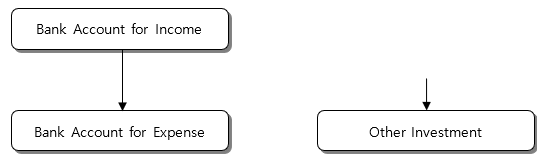

Once business license is released, open the business bank accounts for each purpose separately

① Bank book for the Income

② Bank book for the Expense (open more than one based on the needs)

The purpose of having the separate bank accounts is to manage the property on all in and out of the money flow.

① It is strictly not allowed to use directly from the Income bank account for the Expense spending.

② All spending should be made from Expense bank account after having the money transferred from Income bank account to Expense bank account.

③ It is recommendable to open separate Expense bank account with expense limit according to grade of each manager(s)

In case it is inevitably to use "Private Credit Card" for business purpose before the "Corporate Credit Card" is issued, it is required to use a designated "Private Credit Card" SOLELY for business purpose.

6. Stock Transfer

-

(1) Stock evaluation must be taken before moving stocks pursuant to tax law, inheritance tax, and gift tax

-

(2) Draw up a contract including share transfer agreement and stock certificate contract

-

(3) In case of transfer, filing for transfer gains tax and security transaction tax is required

In case of giving, filing for gift tax is required

-

(4) Where stocks are transferred at a remarkably low price with having huge gap with standard market price it is likely to be regarded as legal fiction of donation

7. Basic ledgers for SME business owners

- Cash book

- Customer's ledger

- Purchase and sales ledger

Advisory & ConsultingBookkeeping ServiceOverview for FDIs

Advisory & ConsultingBookkeeping ServiceOverview for FDIs